|

|

The Insurance Replacement Cost Appraisal also commonly referred to as a Replacement Cost Valuation (RCV) or Insurance-to-Value (ITV), is a report that sets out the cost to reconstruct a particular building or set of buildings and other site improvements in the event of a total loss due to an insurable cause such as hurricane, fire, sinkhole, etc.

It is important to note the land value and total market value are not considered. A current Insurance Replacement Cost Appraisal is an essential aid to you, your broker, your property manager and your insurer in determining the correct insurance limits. |

|

An independent Replacement Cost Appraisal can provide you with a knowledgeable opinion of your building's Replacement Cost Value that is unbiased and is prepared based on your particular building style, construction techniques, and insurance policy. If you are over insured this will result in excess insurance premiums. If you are under insured you may be required to pay a co-insurance penalty in the event of a loss. This report will ensure that you are not paying an extra premium for uninsured items. In many cases certain building components are either not insured or specifically excluded from coverage. The three most common exclusions are: basement excavation; below grade foundations and underground plumbing, piping, and conduits.

|

|

|

|

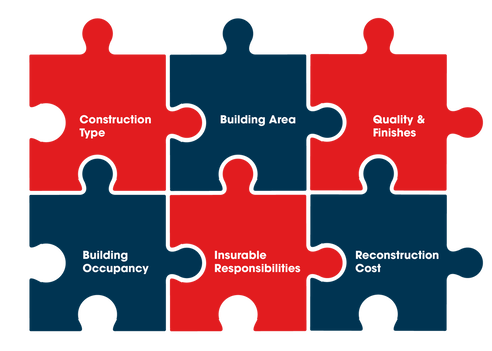

An accurate Insurance Appraisal requires a thorough comprehension of insurance policies, construction techniques and community association structure. Felten Property Assessment Team has developed a tried-and-true methodology of placing emphasis on the six most important key factors which will result in accurate replacement cost, insurance ratings and premiums. The six keys to an accuracy are as follows:

|

Insurance Appraisal Methodology

1. Construction Type - For each building we will identify the building materials used to construct the supporting members of the superstructure. This includes detailed descriptions of the vertical supports, exterior walls, subfloors, and roof deck construction. This vital information will give your insurance broker the information they need to accurately rate your building for fire, wind, and flood insurance.

2. Building Area - Each building will physically measured or building plans will be utilized to determine the exact square footage. We will provide detailed floor-by-floor sketches of each building accurately separating living areas, utility areas, common areas, balconies, and other limited common areas. This information will allow us to value each area at an appropriate cost per square foot. For example: Living areas should be valued at a much higher cost than unfinished utility areas or balconies. Also, in many cases unit owners may be responsible for insuring interior finishes.

3. Building Occupancy - We will accurately identify the occupancy of each building. Is the building a condominium, apartment, cooperative, office, etc. or a combination of multiple occupancies? Each occupancy must be valued at an appropriate cost per square foot. Many multi-family buildings contain parking garages on the first level. These areas should be identified and valued appropriately. All to often we see Insurance Appraisals that do not accurately separate the different occupancies.

4. Quality & Finishes - Determining the appropriate overall construction quality of a building plays a major role when determining an accurate replacement cost estimate. We have inspected buildings of all different occupancies ranging from as low as ten thousand dollars all the way up to hundreds of millions of dollars. Experience is the only way to guarantee quality is accurately determined. The construction quality adjustment to be made is not one of a condominium quality versus an office quality, but rather the quality of the condominium being valued versus the average quality of condominiums. This is why experience matters!

5. Insurable Responsibilities - Our client is the association or the owner of the building not the individual unit owners or tenants. We are preparing the replacement cost valuation for our client. The goal is to determine what the reconstruction cost is for the building components that our client is responsible for insuring. If the building is part of a condominium association we will follow the Florida statutory guidelines for casualty insurance. If the building is part of a homeowners association or other entity we will review the CC&R documents to ensure we are only valuing the components of the building which the association is responsible for insuring. We will ensure that our client does not pay any insurance premiums for items they are not responsible for!

6. Reconstruction Cost Database - Once all of this information is gathered the insurable replacement cost is calculated using a reconstruction cost database. Reconstruction cost is the cost to replicate, at current prices, using like kind and quality materials, construction standards, design/layout, and quality of workmanship. Reconstruction costs also include a number of site-specific and process-related costs that are experienced when rebuilding after a loss. These additional expenses are related to repair/restoration contractors, construction process, time urgency, limited site mobility, adjoining non-construction areas, insured’s property, economies of scale, dangerous/hazardous materials, and mold concerns. Reconstruction cost should not be confused with new construction cost which is used by real estate appraisers. If you hire a real estate appraiser to perform an insurance appraisal make sure they are utilizing a reconstruction cost database!

2. Building Area - Each building will physically measured or building plans will be utilized to determine the exact square footage. We will provide detailed floor-by-floor sketches of each building accurately separating living areas, utility areas, common areas, balconies, and other limited common areas. This information will allow us to value each area at an appropriate cost per square foot. For example: Living areas should be valued at a much higher cost than unfinished utility areas or balconies. Also, in many cases unit owners may be responsible for insuring interior finishes.

3. Building Occupancy - We will accurately identify the occupancy of each building. Is the building a condominium, apartment, cooperative, office, etc. or a combination of multiple occupancies? Each occupancy must be valued at an appropriate cost per square foot. Many multi-family buildings contain parking garages on the first level. These areas should be identified and valued appropriately. All to often we see Insurance Appraisals that do not accurately separate the different occupancies.

4. Quality & Finishes - Determining the appropriate overall construction quality of a building plays a major role when determining an accurate replacement cost estimate. We have inspected buildings of all different occupancies ranging from as low as ten thousand dollars all the way up to hundreds of millions of dollars. Experience is the only way to guarantee quality is accurately determined. The construction quality adjustment to be made is not one of a condominium quality versus an office quality, but rather the quality of the condominium being valued versus the average quality of condominiums. This is why experience matters!

5. Insurable Responsibilities - Our client is the association or the owner of the building not the individual unit owners or tenants. We are preparing the replacement cost valuation for our client. The goal is to determine what the reconstruction cost is for the building components that our client is responsible for insuring. If the building is part of a condominium association we will follow the Florida statutory guidelines for casualty insurance. If the building is part of a homeowners association or other entity we will review the CC&R documents to ensure we are only valuing the components of the building which the association is responsible for insuring. We will ensure that our client does not pay any insurance premiums for items they are not responsible for!

6. Reconstruction Cost Database - Once all of this information is gathered the insurable replacement cost is calculated using a reconstruction cost database. Reconstruction cost is the cost to replicate, at current prices, using like kind and quality materials, construction standards, design/layout, and quality of workmanship. Reconstruction costs also include a number of site-specific and process-related costs that are experienced when rebuilding after a loss. These additional expenses are related to repair/restoration contractors, construction process, time urgency, limited site mobility, adjoining non-construction areas, insured’s property, economies of scale, dangerous/hazardous materials, and mold concerns. Reconstruction cost should not be confused with new construction cost which is used by real estate appraisers. If you hire a real estate appraiser to perform an insurance appraisal make sure they are utilizing a reconstruction cost database!